Filing Your Income Tax Return on Time Matters More Than You Think

Every financial year, millions of taxpayers wait until the last few days to file their Income Tax Return (ITR). Some assume they have plenty of time, while others believe that if no tax is payable, filing an ITR isn't necessary.

However, missing the due date can lead to unnecessary penalties, interest charges, delayed refunds, and even the loss of certain tax benefits.

For the Financial Year 2025–26 (Assessment Year 2026–27), the Income Tax Department has enabled online filing for eligible taxpayers and announced different due dates depending on the type of taxpayer and return being filed.

This guide explains all the important ITR deadlines, who needs to file by when, what happens if you miss the due date, and the options available even after the deadline.

Latest Update for AY 2026–27

The Income Tax Department has started accepting Income Tax Returns for Assessment Year 2026–27.

Currently, the filing utilities are available for:

- ITR-1

- ITR-2

- ITR-4

Eligible taxpayers can file their returns through the Income Tax e-filing portal before the applicable due date.

If you miss the original deadline, you may still have the option to file a belated return or an updated return, subject to the provisions of the Income Tax Act.

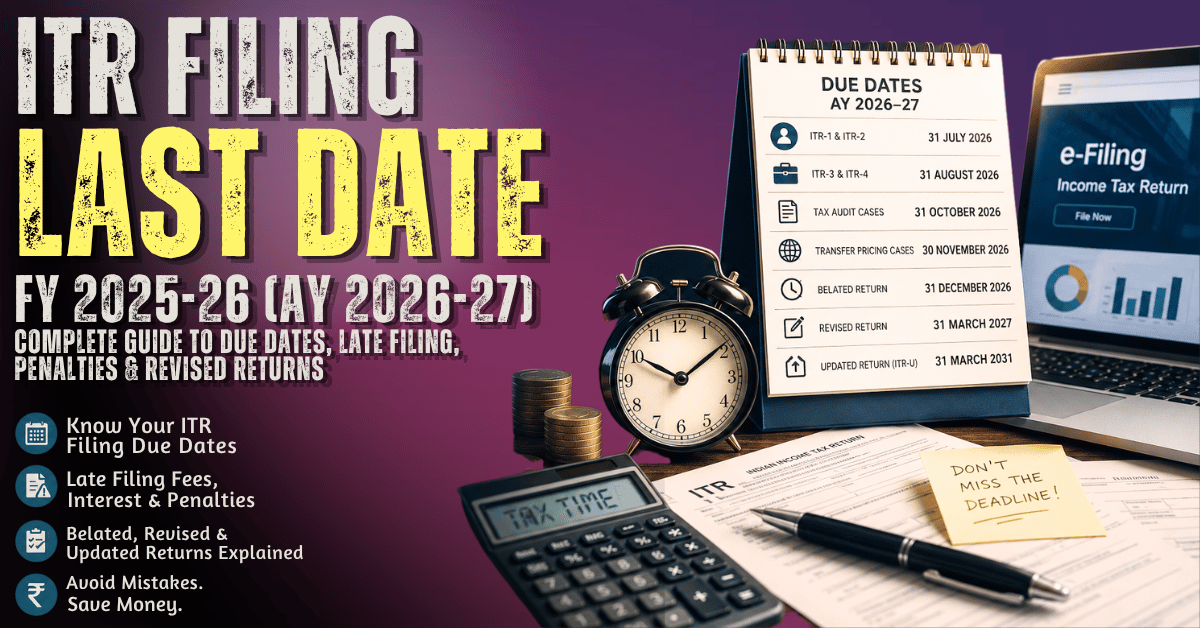

ITR Filing Due Dates for FY 2025–26 (AY 2026–27)

Different taxpayers have different filing deadlines. Your due date depends on the nature of your income and whether your accounts require a tax audit.

|

Category |

Due Date |

|

ITR-1 & ITR-2 (Salary, Pension, Capital Gains) |

31 July 2026 |

|

ITR-3 & ITR-4 (Business/Profession – Non-Audit Cases) |

31 August 2026 |

|

Businesses Requiring Tax Audit |

31 October 2026 |

|

Transfer Pricing Cases |

30 November 2026 |

|

Belated Return |

31 December 2026 |

|

Revised Return |

31 March 2027 |

|

Updated Return (ITR-U) |

31 March 2031 |

Note: These dates apply unless the Income Tax Department announces an extension.

Which ITR Form Should You File?

Choosing the correct ITR form is just as important as filing on time.

ITR-1

Suitable for resident individuals earning income from:

- Salary or pension

- One house property

- Other sources (such as interest income)

- Agricultural income up to the prescribed limit

ITR-2

Applicable to individuals and HUFs who:

- Earn capital gains

- Own multiple house properties

- Have foreign assets or foreign income

- Are not carrying on business or profession

ITR-3

Designed for taxpayers having income from:

- Proprietorship business

- Professional practice

- Partnership firms

- Other business activities

ITR-4

Applicable for taxpayers opting for the presumptive taxation scheme under eligible sections.

Can You File ITR After the Due Date?

Yes.

Missing the original due date does not always mean you lose the opportunity to file your return.

The Income Tax Act provides two additional options depending on your situation:

- Belated Return

- Updated Return (ITR-U)

Let's understand both.

What Is a Belated Return?

A belated return is filed after the original due date but before the prescribed deadline.

For AY 2026–27, taxpayers can file a belated return until 31 December 2026.

However, filing late may result in:

- Late filing fees

- Interest on unpaid tax

- Delay in receiving refunds

- Loss of certain tax benefits

Although filing late is better than not filing at all, taxpayers should always aim to file within the original due date.

What Is an Updated Return (ITR-U)?

The Updated Return (ITR-U) was introduced to encourage voluntary tax compliance.

If you missed both the original due date and the belated return deadline, you may still be eligible to file an Updated Return.

For AY 2026–27, taxpayers can file ITR-U until 31 March 2031, subject to prescribed conditions.

An Updated Return can be filed whether or not you filed an original return earlier.

However:

- It cannot be used to claim additional refunds.

- It cannot be used to increase losses.

- Once filed, it cannot be revised again.

Belated Return vs Updated Return

|

Particular |

Belated Return |

Updated Return |

|

Filed When |

Original due date is missed |

Original and belated due dates are both missed |

|

Last Date (AY 2026–27) |

31 December 2026 |

31 March 2031 |

|

Late Fees |

Applicable |

Additional tax payable as per law |

|

Can Be Revised |

Applicable |

No |

Made a Mistake After Filing Your Return?

Mistakes can happen.

You may discover later that:

- You forgot to claim a deduction.

- You entered incorrect bank details.

- Some income was left out.

- Capital gains were reported incorrectly.

Fortunately, the Income Tax Act allows eligible taxpayers to correct such mistakes through a Revised Return.

What Is a Revised Return?

A revised return allows taxpayers to rectify errors made in the original Income Tax Return.

For AY 2026–27, a revised return can generally be filed until 31 March 2027.

Example

Suppose you filed your return in June 2026.

Later, in August 2026, you realised that you forgot to claim a deduction under Section 80C.

Instead of filing a fresh return, you can simply submit a revised return before the applicable deadline.

What Happens If You Miss the ITR Filing Deadline?

Ignoring the due date can have financial as well as practical consequences.

1. Interest on Outstanding Tax

If any tax remains unpaid, interest under Section 234A is generally charged at 1% per month or part of a month until the tax liability is cleared.

2. Late Filing Fee

Late filing may attract a fee under Section 234F.

Generally:

- ₹5,000 if total income exceeds ₹5 lakh.

- ₹1,000 if total income is up to ₹5 lakh.

3. Loss of Carry Forward Benefits

Taxpayers who incur:

- Business losses

- Capital losses

may lose the ability to carry those losses forward to future years if the return is not filed within the prescribed due date.

This could result in higher tax liability in future years.

4. Delay in Income Tax Refund

If you are eligible for a refund, filing late may delay its processing.

The earlier you file an accurate return, the sooner your refund is generally processed.

5. Impact on Financial Credibility

An Income Tax Return is often required while applying for:

- Home loans

- Business loans

- Personal loans

- Credit cards

- Visa applications

Delayed or non-filing may create unnecessary complications during document verification.

Income Tax Act 1961 vs Income Tax Act 2025

Although the Income Tax Act, 2025 comes into force from 1 April 2026, returns for Assessment Year 2026–27 continue to be governed by the provisions applicable to income earned during FY 2025–26.

Some section numbers have changed under the new Act.

|

Topic |

Income Tax Act, 1961 |

Income Tax Act, 2025 |

|

Interest for Late Filing |

Section 234A |

Section 423 |

|

Late Filing Fee |

Section 234F |

Section 428 |

|

Belated Return |

Section 139(4) |

Section 263(4) |

|

Revised Return |

Section 139(5) |

Corresponding provision under the 2025 Act |

Tips to File Your ITR on Time

Before submitting your return, make sure you:

- Collect Form 16, AIS, Form 26AS, and other income documents.

- Verify bank account details.

- Report all sources of income.

- Claim only eligible deductions.

- Cross-check tax payments and TDS credits.

- E-verify your return after filing to complete the process.

Final Thoughts

Filing your Income Tax Return before the due date is one of the simplest ways to stay compliant, avoid unnecessary penalties, and maintain a strong financial record. Whether you are a salaried employee, freelancer, professional, or business owner, timely filing can help you receive faster refunds, preserve tax benefits, and simplify future financial transactions.

If you miss the original deadline, the law still provides options such as belated returns, revised returns, and Updated Returns (ITR-U). However, these alternatives may involve additional costs or restrictions, making timely filing the most beneficial approach.

Comments

No comments yet. Be the first to comment!