The Income Tax Return Filing Process Has Changed—Here's Everything You Need to Know Before Filing Your ITR

The Income Tax Return (ITR) filing season for Financial Year 2025–26 (Assessment Year 2026–27) has officially begun, bringing several important updates that taxpayers should understand before filing their returns.

This year, the Income Tax Department has introduced revised ITR forms, updated filing timelines, enhanced disclosure requirements for Futures & Options (F&O) traders, and new compliance measures aimed at improving transparency and reducing filing errors.

Whether you are a salaried employee, freelancer, business owner, investor, or active stock market trader, understanding these latest changes is essential for filing an accurate return, avoiding notices, and ensuring timely tax compliance.

In this article, we explain all the major updates introduced for FY 2025–26 in simple language.

Why These Changes Matter

Every financial year, the Income Tax Department updates return forms and filing procedures to align with amendments made in the Income Tax Act and to improve tax reporting.

The changes introduced for FY 2025–26 focus on:

- Simplifying return filing

- Improving transparency

- Better reporting of financial transactions

- Reducing incorrect claims

- Encouraging voluntary tax compliance

Taxpayers who continue filing returns using old assumptions may end up making mistakes that could lead to defective returns, delayed refunds, or even scrutiny notices.

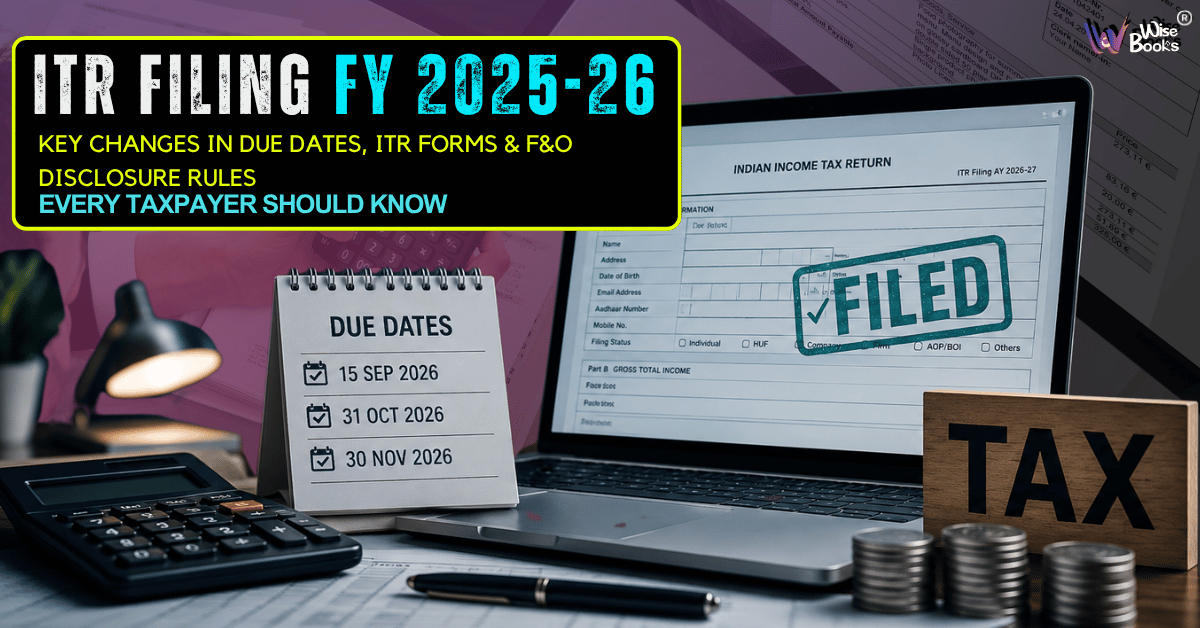

1. Revised Due Dates for Filing ITR

One of the biggest changes this year is the revised filing schedule.

Unlike previous years where most taxpayers focused only on the July deadline, different categories of taxpayers now have different due dates depending on the nature of income and audit requirements.

Expected Due Dates

|

Category |

Due Date |

|

Individual taxpayers not requiring audit |

15 September 2026 |

|

Businesses requiring tax audit |

31 October 2026 |

|

Taxpayers covered under transfer pricing |

30 November 2026 |

|

Updated Return (ITR-U) |

Up to 48 months from relevant assessment year (subject to conditions) |

Why This Is Important

Many taxpayers assume that everyone must file by the same date. However, filing after your applicable due date can result in:

- Late filing fees

- Interest on outstanding taxes

- Delay in refund processing

- Loss of certain tax benefits

- Carry-forward restrictions for certain losses

Knowing your applicable deadline helps you avoid unnecessary penalties.

2. New ITR Forms Introduced for FY 2025–26

The Income Tax Department has revised several ITR forms to improve disclosure requirements and simplify reporting.

These forms now capture more detailed financial information while removing unnecessary reporting requirements in certain cases.

Key Improvements

The revised forms now include:

i. Better reporting of capital gains

ii. Updated deduction schedules

iii. Improved asset disclosure

iv. More detailed reporting for business income

v. Enhanced verification of tax credits

vi. Better reporting of exempt income

These modifications are intended to reduce mismatches between taxpayer declarations and information already available with the department.

3. Staggered Release of ITR Utilities

Another noticeable change this year is the phased release of ITR utilities.

Instead of releasing all return filing utilities simultaneously, the Income Tax Department has made different ITR forms available at different times.

What This Means for Taxpayers

Many taxpayers may notice that their preferred ITR form is not immediately available.

This staggered rollout allows the department to ensure technical stability and incorporate updates before all forms become available for filing.

Taxpayers should verify whether their respective ITR utility has been released before beginning the filing process.

4. Major Changes in ITR-3 for Business Owners and Professionals

The revised ITR-3 now requires more comprehensive disclosures from taxpayers earning business or professional income.

The objective is to capture financial information more accurately and improve tax reporting.

Additional Reporting May Include

- Business turnover

- Profit computation

- Balance sheet details

- Loan information

- Asset reporting

- Tax audit information

- Presumptive taxation disclosures where applicable

Taxpayers filing ITR-3 should carefully review every schedule before submission.

5. Important Changes in ITR-4 (Sugam)

Taxpayers opting for presumptive taxation under Sections 44AD, 44ADA, or 44AE should carefully review the revised ITR-4.

The form now contains additional reporting fields aimed at ensuring that taxpayers claiming presumptive taxation satisfy all eligibility conditions.

Who Uses ITR-4?

Generally:

- Small business owners

- Professionals under presumptive taxation

- Small transport businesses

The revised form is expected to improve consistency between reported income and actual financial transactions.

6. New Disclosure Rules for Futures & Options (F&O) Traders

One of the most significant changes this year relates to taxpayers involved in Futures & Options (F&O) trading.

The Income Tax Department now expects more comprehensive reporting of derivatives transactions.

Why the New Disclosure Rules?

Over the past few years, participation in stock derivatives has increased significantly.

To improve transparency and minimize incorrect reporting, taxpayers engaged in F&O trading are expected to disclose more detailed information regarding their trading activities.

What Information May Need to Be Reported?

Depending on the applicable return form and nature of business, taxpayers may need to disclose:

- Gross turnover from F&O

- Net profit or loss

- Trading expenses

- Audit applicability

- Presumptive taxation eligibility (if applicable)

- Financial statements

Maintaining accurate trading records has become increasingly important.

7. Better Reporting of Capital Gains

Capital gains reporting has also become more structured.

Taxpayers selling:

- Shares

- Mutual funds

- Property

- Bonds

- Securities

should carefully classify transactions under the correct capital gains schedules.

Accurate reporting ensures faster processing and reduces the possibility of tax notices.

8. Enhanced Cross-Verification by the Income Tax Department

The Income Tax Department now receives financial information from multiple reporting entities.

These include:

- Banks

- Employers

- Mutual fund houses

- Stock brokers

- Registrars

- Property registrars

- Financial institutions

As a result, discrepancies between reported income and available financial information can be detected more easily.

Taxpayers should therefore reconcile all financial data before filing their returns.

9. Verify Your Annual Information Statement (AIS) Before Filing

One of the most important steps before filing your ITR is reviewing your Annual Information Statement (AIS).

The AIS contains details such as:

- Salary

- Interest income

- Dividend income

- Securities transactions

- Mutual fund investments

- Tax deducted at source (TDS)

- Property transactions

- High-value financial transactions

Matching your return with the AIS helps reduce errors and minimizes the chances of receiving compliance notices.

10. Choose the Correct ITR Form

Selecting the wrong ITR form remains one of the most common filing mistakes.

The appropriate form depends on factors such as:

- Salary income

- Business income

- Professional income

- Capital gains

- Rental income

- Foreign assets

- Agricultural income

- Presumptive taxation

Using an incorrect return form may result in the return being treated as defective.

11. Keep Supporting Documents Ready

Although most documents are not uploaded while filing the return, taxpayers should keep them readily available.

These include:

- Form 16

- Form 26AS

- AIS

- TIS

- Bank statements

- Investment proofs

- Capital gains statements

- Interest certificates

- Home loan certificates

- Business financial records

Maintaining proper documentation makes filing easier and helps during any future verification.

12. Common Mistakes Taxpayers Should Avoid

Many taxpayers unintentionally make errors while filing their returns.

Some common mistakes include:

- Selecting the wrong ITR form

- Reporting incorrect bank account details

- Missing additional income

- Ignoring capital gains

- Claiming ineligible deductions

- Failing to reconcile TDS

- Not verifying the return after submission

Careful review before final submission can prevent delays and notices.

How These Changes Affect Different Taxpayers

For Salaried Employees

Most salaried individuals will benefit from improved reporting and simplified return forms, but they should verify salary, TDS, and investment details before filing.

For Business Owners

Businesses should maintain updated books of accounts and ensure that turnover, expenses, and financial statements match the information reported in the return.

For Professionals

Professionals opting for presumptive taxation should review eligibility conditions carefully before filing ITR-4.

For Stock Market Traders

Active traders, especially those dealing in Futures & Options, should maintain detailed transaction records, calculate turnover correctly, and ensure accurate disclosure of profits, losses, and expenses to comply with the revised reporting requirements.

Benefits of Filing Your ITR Early

Rather than waiting until the last date, filing early offers several advantages:

- Faster refund processing

- More time to correct mistakes

- Reduced last-minute technical issues

- Easier tax planning

- Lower risk of penalties due to missed deadlines

Early filing also provides peace of mind and ensures timely compliance.

Final Thoughts

The Income Tax Return filing process for FY 2025–26 (AY 2026–27) introduces several noteworthy changes that taxpayers should not overlook. From revised filing due dates and updated ITR forms to enhanced reporting for business income and Futures & Options (F&O) transactions, these changes are designed to improve transparency, strengthen compliance, and simplify return processing.

Before filing your return, review your financial records, reconcile your income with Form 26AS, the Annual Information Statement (AIS), and the Taxpayer Information Summary (TIS), choose the correct ITR form, and verify all disclosures carefully. Staying informed and filing accurately can help you avoid penalties, reduce the risk of notices, and ensure faster processing of refunds.

With proper preparation and timely action, taxpayers can complete the ITR filing process confidently while remaining fully compliant with the latest income tax requirements.

Comments

No comments yet. Be the first to comment!