The Goods and Services Tax Network (GSTN) has rolled out a structured online mechanism enabling eligible taxpayers registered under Rule 14A of the CGST Rules to withdraw (opt out) from the option earlier availed. The facility, effective from 21 February 2026, allows filing of Form GST REG-32 directly on the GST Portal, subject to defined eligibility conditions, Aadhaar authentication requirements, and compliance safeguards.

This development strengthens procedural transparency while ensuring that only compliant taxpayers can exit the Rule 14A framework.

Background: What Rule 14A Signifies

Rule 14A governs a specific category of GST registration mechanism under the CGST Rules. Taxpayers who opted into this structure were subject to particular reporting and operational conditions prescribed under the law.

Over time, certain registered persons may seek to withdraw from this option due to operational restructuring, compliance alignment, business scale changes, or regulatory considerations. Until now, the process lacked a clearly automated exit pathway. The new GSTN functionality provides a formal digital channel for such withdrawal.

Who Can Apply for Withdrawal

The withdrawal facility is not universally available to all registered persons. It is accessible only to:

- Taxpayers whose registration status is Active

- Persons currently registered under Rule 14A

- Those meeting prescribed return filing conditions

- Applicants completing mandatory Aadhaar authentication

The withdrawal link becomes visible in the GST Portal dashboard only when these system-validated conditions are satisfied.

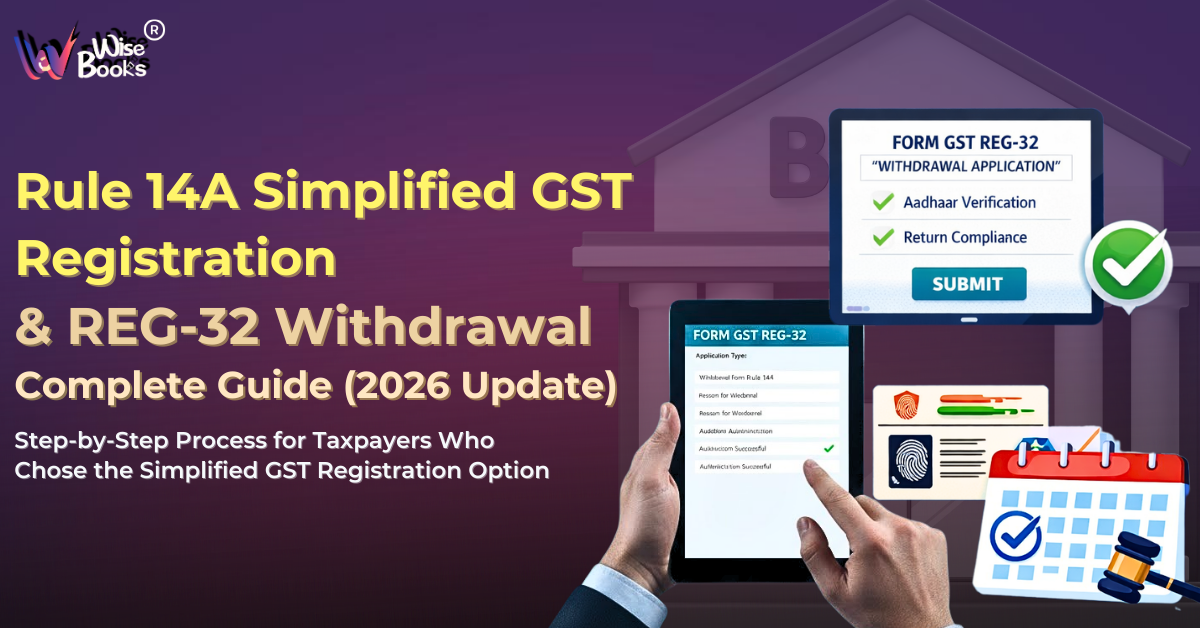

Online Filing Process Through GST Portal

The withdrawal request must be filed electronically using Form GST REG-32.

After logging into the GST Portal, taxpayers must navigate to:

Services → Registration → Application for Withdrawal from Rule 14A

The system auto-populates the registration option as “No” (indicating opt-out intent). The applicant is required to provide a reason for withdrawal before proceeding to Aadhaar authentication.

The Application Reference Number (ARN) is generated only after successful completion of authentication procedures.

Return Filing Preconditions Before Submission

To ensure compliance discipline, GSTN has imposed minimum return filing thresholds before REG-32 can be submitted.

Applications Filed Before 1 April 2026

The taxpayer must have filed returns for a minimum period of three months.

Applications Filed On or After 1 April 2026

The taxpayer must have filed returns for at least one tax period.

In both cases, all pending returns from the effective date of registration until the date of application must be furnished. If any return remains pending, the system blocks submission.

This condition ensures that only compliant taxpayers can opt out and prevents misuse of procedural flexibility.

Aadhaar Authentication Framework

A significant compliance safeguard built into the withdrawal process is Aadhaar authentication.

Based on risk parameters and system analytics, the portal may require either:

- OTP-based Aadhaar authentication, or

- Biometric-based Aadhaar authentication.

Authentication is mandatory for:

- The Primary Authorised Signatory

- At least one Promoter or Partner, wherever applicable

If authentication is not completed successfully within the prescribed timeline, the ARN will not be generated and the application will lapse automatically.

This risk-based verification mechanism is consistent with the broader GST digital compliance architecture aimed at curbing identity misuse.

Time Limits and Application Validity

The withdrawal process under Rule 14A operates within clearly defined timelines to maintain procedural discipline and system efficiency.

A draft of Form GST REG-32 must be submitted within 15 days from the date it is created. If the draft remains incomplete beyond this period, it automatically lapses on the portal.

Further, Aadhaar or biometric authentication must be completed within 15 days from the date of submission. Since ARN is generated only after successful authentication, any delay in completing this step results in the application becoming invalid.

If these deadlines are not met, the taxpayer must initiate a fresh application, subject to re-validation of eligibility conditions at that time. These structured timelines ensure transparency, prevent indefinite pendency, and support streamlined digital governance under GST.

Restrictions During Processing of REG-32

Once Form GST REG-32 is submitted, the application enters a processing stage, during which certain system-based restrictions are automatically triggered on the GST portal.

During this period:

i. Core amendments (such as changes in legal name, principal place of business, partners, or authorised signatories) cannot be filed.

ii. Non-core amendments are either restricted or temporarily disabled.

iii. Application for cancellation of registration cannot be submitted.

These temporary restrictions are designed to maintain consistency in the taxpayer’s registration profile while the withdrawal request is under examination by the proper officer. Allowing simultaneous amendments or cancellation could create inconsistencies in records, affect verification checks, or complicate the approval process.

By freezing structural changes during processing, the system ensures procedural clarity, avoids overlapping compliance actions, and supports a smooth regulatory assessment under GST.

Post-Approval Consequences and Compliance Implications

Upon examination and approval by the proper officer, an order is issued in Form GST REG-33.

Following approval:

- Withdrawal becomes effective.

- The taxpayer is permitted to furnish output tax liability details exceeding ₹2.5 lakh on supplies made to registered persons.

- Such reporting becomes applicable from the first day of the succeeding month in which the withdrawal order is issued.

This ensures a clean transition from the Rule 14A framework to the standard GST reporting structure.

Regulatory Significance of This Update

The automated withdrawal facility under Rule 14A is more than a portal upgrade — it reflects the evolving compliance framework of GST.

i. Digitised Governance:

The entire process is system-driven, reducing manual intervention and ensuring uniform treatment across jurisdictions.

ii. Risk-Based Verification:

Mandatory Aadhaar authentication strengthens identity validation and prevents misuse of registration mechanisms.

iii. Return-Linked Eligibility:

Withdrawal is allowed only after prescribed return filing, reinforcing the principle that procedural benefits are tied to compliance discipline.

iv. Time-Bound Processing:

Defined 15-day timelines prevent indefinite pendency and improve administrative efficiency.

Overall, the update integrates flexibility with structured digital compliance, aligning procedural ease with regulatory control.

Practical Considerations for Taxpayers

Before applying for withdrawal under Rule 14A, businesses should review a few important compliance aspects.

Return Filing Status

All GST returns from the effective date of registration must be filed and reconciled. Even one pending return will prevent submission of Form GST REG-32.

Aadhaar Readiness

Ensure Aadhaar details of the Primary Authorised Signatory and at least one Promoter/Partner are valid and accessible for OTP or biometric authentication to avoid delay in ARN generation.

Business Justification

Evaluate whether opting out aligns with operational structure and compliance strategy, as withdrawal should be a considered decision.

Processing Restrictions

Once REG-32 is filed, amendments and self-cancellation cannot be made until the application is disposed of.

Proper planning helps avoid rejection, delay, or lapse of the application.

Conclusion

The GSTN’s introduction of the Rule 14A withdrawal facility through Form GST REG-32 represents a structured compliance reform in 2026. While the process is now fully digitised, it is governed by clear eligibility conditions, Aadhaar authentication mandates, return filing prerequisites, and defined timelines.

Taxpayers intending to opt out must approach the process with complete procedural preparedness to ensure seamless approval and avoid unnecessary compliance hurdles.

Comments

No comments yet. Be the first to comment!