The Goods and Services Tax Appellate Tribunal (GSTAT) has introduced a significant relief mechanism for taxpayers who are unable to complete the online filing of GST appeals before the statutory deadline.

Recognizing that many taxpayers and professionals may face technical or procedural difficulties while filing appeals on the GSTAT portal, the Tribunal has launched a Token Generation Mechanism. This facility allows eligible appellants to record their intention to file an appeal before the due date and complete the filing later, subject to specified conditions. The mechanism has been introduced under Order No. 156/2026 dated 10 July 2026 in exercise of the powers under Rule 123 of the GST Appellate Tribunal (Procedure) Rules, 2025.

This is a welcome step for businesses, tax professionals, and taxpayers with pending GST disputes, as it reduces the risk of losing the right to appeal due to last-minute filing issues.

Why Was the Token Generation Mechanism Introduced?

The GST Appellate Tribunal has recently become operational, and thousands of taxpayers are expected to file appeals within a short period. The surge in filings has led to concerns regarding portal congestion and technical challenges. The Government had already extended the deadline for certain appeals from 30 June 2026 to 31 July 2026, and the token mechanism now provides an additional safeguard for those facing genuine filing difficulties.

The objective is simple:

- Ensure taxpayers do not lose their right to appeal due to portal-related issues.

- Reduce last-minute pressure on the GSTAT portal.

- Provide sufficient time to complete appeal documentation after recording the intention to appeal.

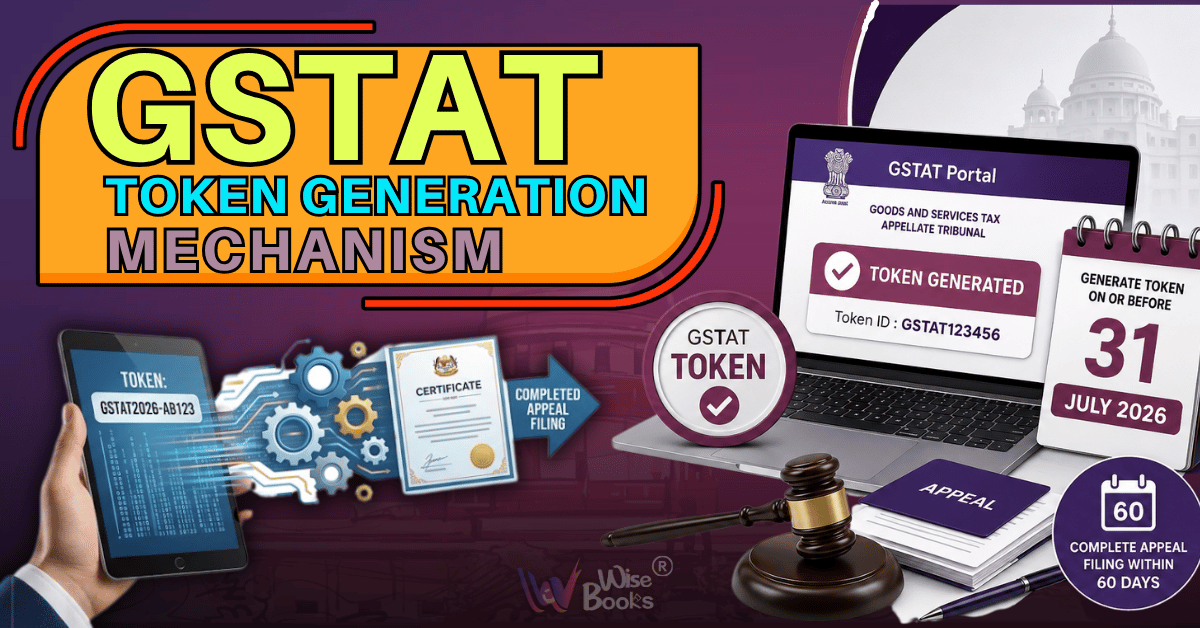

What Is a GSTAT Token?

A GSTAT Token is an electronically generated acknowledgement that records an appellant's intention to file an appeal before the GST Appellate Tribunal.

It is important to understand that the token is not the appeal itself. Instead, it serves as proof that the appellant attempted to initiate the appeal within the prescribed time limit.

The actual appeal, along with all supporting documents, must still be filed separately within the prescribed period.

Important Deadlines

Step 1: Generate the Token

Eligible taxpayers who wish to file an appeal should generate their token on or before 31 July 2026.

This records their intention to file the appeal within the statutory time limit.

Step 2: Complete the Appeal Filing

Once the token is generated, the appellant has 60 days from the date of token generation to submit the complete appeal on the GSTAT portal.

For example:

- Token generated on 20 July 2026

- Last date for complete appeal filing: 18 September 2026

Similarly,

- Token generated on 31 July 2026

- Last date for complete appeal filing: 29 September 2026

Who Can Use This Facility?

The token mechanism is intended for appellants filing appeals under Section 112 of the CGST Act, 2017, particularly those who encounter technical or procedural difficulties while completing the online filing process.

The advisory applies to taxpayers, authorised representatives, and other eligible appellants covered by the notified transition arrangements.

How Does the Token Generation Process Work?

The process is straightforward:

1. Visit the GSTAT e-filing portal.

2. Access the Token Generation form.

3. Fill in the minimum mandatory details relating to the appeal.

4. Submit the request.

5. A unique Token ID along with the date and time of generation will be issued.

6. Preserve the Token ID carefully.

7. Complete the appeal filing within 60 days.

The Token ID acts as evidence that the appellant initiated the appeal process before the due date.

Important Conditions You Should Know

While the mechanism provides welcome relief, it comes with important conditions:

The token is not a substitute for the appeal

Generating a token alone does not complete the appeal process.

Appeal must be filed within 60 days

Failure to complete the appeal within 60 days from token generation will result in the token lapsing.

Separate token for each appeal

If multiple appeals are to be filed, a separate token must be generated for each case.

Correct information is mandatory

Any token generated with incomplete, incorrect, or inaccurate information may be treated as invalid.

What Happens If You Miss the Deadline?

If you fail to generate the token by 31 July 2026, and your appeal is otherwise subject to this transitional deadline, you may lose the benefit of the special relaxation.

Likewise, if you generate the token but do not complete the appeal within 60 days, the token will automatically lapse and cannot be used to preserve the filing timeline.

Benefits of the Token Mechanism

The newly introduced system offers several practical benefits:

- Protects the taxpayer's right to appeal.

- Reduces the impact of technical glitches and portal congestion.

- Gives additional time to prepare documents and grounds of appeal.

- Ensures smoother digital filing before the GST Appellate Tribunal.

- Minimizes the risk of disputes over limitation where the prescribed conditions are fulfilled.

What Should Businesses Do Now?

Businesses with pending GST disputes should not wait until the last day.

Instead, they should:

- Review whether their appeal falls within the notified category.

- Prepare all appeal documents in advance.

- Generate the token well before 31 July 2026, especially if facing filing issues.

- Complete the appeal filing within 60 days.

- Keep a copy of the Token ID and acknowledgement for future reference.

Taking these steps early can help avoid unnecessary litigation risks and ensure compliance with the GSTAT filing requirements.

Final Thoughts

The GSTAT Token Generation Mechanism is a practical and taxpayer-friendly initiative designed to protect appellants during the transition to the Tribunal's online filing system. By allowing taxpayers to record their intention to appeal before the deadline, the Tribunal has addressed concerns around portal congestion and last-minute filing challenges.

However, taxpayers should remember that the token is only a procedural safeguard, it does not replace the appeal itself. To benefit from this relaxation, appellants must generate the token on or before 31 July 2026 and complete the appeal within 60 days of token generation, while complying with all conditions laid down in the GSTAT Order and Advisory.

Comments

No comments yet. Be the first to comment!