Introduction

Every financial year brings new compliance responsibilities for GST-registered businesses, but some updates are more significant than they initially appear. One such important development is the revision of the Aggregate Annual Turnover (AATO) amendment timeline for FY 2025–26.

The Goods and Services Tax Network (GSTN) has introduced an upgraded system that changes not only when taxpayers can amend their turnover but also how the GST portal will manage turnover information in the future. While many businesses may view this as just another portal update, the reality is that your Aggregate Annual Turnover determines several important GST compliances.

If your turnover is incorrect on the GST portal, it could affect return filing frequency, eligibility under various GST schemes, e-invoicing obligations, and other system-driven compliances.

For businesses, accountants, tax professionals, and finance teams, this is the final opportunity to ensure that the GST portal reflects accurate turnover information for FY 2025–26.

What is the Latest GST Update?

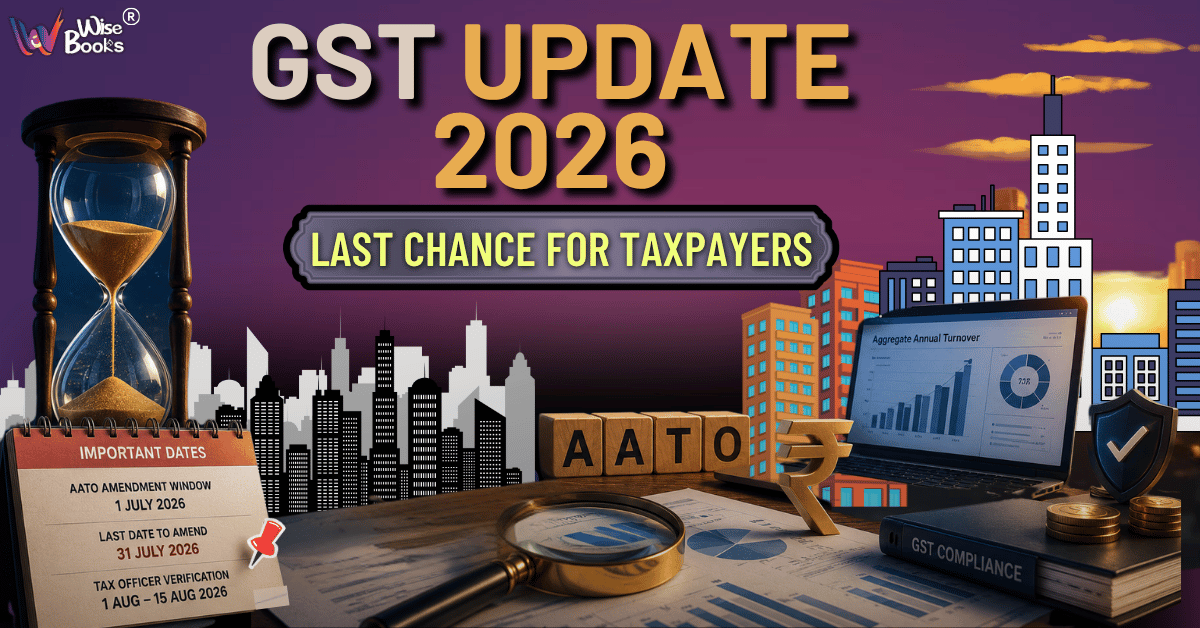

GSTN has revised the timeline for amendment of Aggregate Annual Turnover (AATO) for FY 2025–26 through Advisory No. 666 dated 1 July 2026.

Unlike previous years, taxpayers will no longer get the amendment facility during May. Instead, the amendment window has been shifted to July because GSTN is implementing a more advanced system capable of automatically updating turnover after future GST returns are filed.

Revised Timeline

|

Activity |

Revised Date |

|

AATO Amendment Window Opens |

1 July 2026 |

|

Last Date to Amend |

31 July 2026 |

|

Verification by Tax Officer |

1 August – 15 August 2026 |

Once the amendment window closes, taxpayers cannot make manual corrections for FY 2025–26 through this facility.

What is Aggregate Annual Turnover (AATO)?

Aggregate Annual Turnover (AATO) is the total value of all supplies made by a business under the same Permanent Account Number (PAN) across India during a financial year. It is one of the most important figures under the GST regime because it helps determine whether a taxpayer is required to comply with certain GST provisions, such as e-invoicing, return filing requirements, and other threshold-based compliances.

The GST Portal automatically calculates the AATO based on the GST returns filed by the taxpayer. However, this system-generated turnover may sometimes differ from the actual turnover due to delayed return filing, amendments, reporting errors, or changes in business structure. Therefore, taxpayers should always review the auto-calculated turnover to ensure it accurately reflects their business transactions.

It generally includes:

- Taxable supplies

- Zero-rated supplies (exports and SEZ supplies)

- Exempt supplies

- Inter-state supplies

- Supplies made through different GST registrations under the same PAN

However, it excludes:

- GST collected on supplies

- Inward supplies liable to Reverse Charge

- Certain prescribed transactions excluded under GST law

Why Has GSTN Changed the Timeline?

This isn't merely a date change.

GSTN is introducing an upgraded AATO functionality that will:

- Automatically update turnover when future GST returns are filed.

- Improve consistency across GST modules.

- Reduce manual corrections.

- Improve data accuracy.

- Minimise mismatches across GST records.

Previously, turnover became relatively static after the amendment window. The new functionality is intended to keep AATO more accurate over time as additional returns are filed.

Why Does AATO Matter So Much?

Many taxpayers assume Aggregate Annual Turnover is simply a reporting figure.

In reality, it drives several GST compliances.

A correct AATO determines:

1. E-Invoicing Applicability

Crossing the notified turnover threshold can make e-invoicing mandatory. Incorrect turnover may lead to non-compliance or unnecessary implementation.

2. Composition Scheme Eligibility

Businesses near the turnover limit must ensure their AATO is accurate because eligibility for the Composition Scheme depends on turnover thresholds.

3. Return Filing Requirements

The GST Portal uses turnover information for system-based validations and compliance requirements, which can affect return filing obligations.

4. Portal-Based Validations

Several GST portal functionalities rely on AATO to determine compliance obligations and eligibility.

5. Departmental Risk Assessment

Incorrect turnover data may trigger notices, scrutiny, or requests for clarification during departmental verification.

Who Should Review Their AATO?

Every registered GST taxpayer should review the Aggregate Annual Turnover displayed on the GST Portal, regardless of the size of the business. Even if the turnover appears correct, a quick verification can help identify any hidden discrepancies before the amendment window closes.

You should pay special attention if:

GST Returns Were Filed Late

Delayed filing of returns may affect the turnover automatically computed by the GST Portal.

Previous Returns Were Amended

Changes made after the original filing may not always be reflected accurately without verification.

Turnover Differs from Audited Financial Statements

If your books of accounts and GST Portal show different turnover figures, reconciliation becomes necessary.

Business Restructuring Took Place

Mergers, demergers, business transfers, or changes in organisational structure can impact turnover reporting.

Multiple GST Registrations Exist Under One PAN

Businesses operating in multiple states should verify that turnover from all registrations has been correctly aggregated.

Sales Figures Were Revised During the Year

Corrections made to invoices or turnover should be reflected accurately in the portal.

Export Figures Were Modified

Businesses involved in exports should ensure that zero-rated supplies are correctly included in the turnover.

Errors Occurred While Filing GST Returns

Mistakes in GSTR-1 or GSTR-3B can result in inaccurate turnover calculations.

What Happens If You Ignore This Update?

Failure to review AATO before the deadline may result in:

- Incorrect GST compliance obligations.

- Wrong determination of threshold-based provisions.

- Possible GST notices due to turnover mismatches.

- Compliance issues during audits.

- Additional administrative effort to rectify discrepancies later.

While this amendment window is not a tax payment deadline, it is an important compliance opportunity that can influence future GST obligations.

Step-by-Step Process to Review and Amend AATO

Taxpayers should complete the following steps before the prescribed deadline:

Step 1: Log in to the GST Portal using your credentials.

Step 2: Navigate to the Aggregate Annual Turnover (AATO) section available

Step 3: Compare the turnover displayed on the portal with your books of accounts, audited financial statements, and GST returns.

Step 4: Identify any differences or reporting errors that require correction.

Step 5: Submit the amendment request, if necessary, before 31 July 2026.

Step 6: Preserve all supporting documents and reconciliations for future verification.

The amended turnover will be examined by the jurisdictional tax officer during the verification period from 1 August to 15 August 2026.

Common Reasons for Turnover Mismatches

Turnover differences may arise for several practical reasons, including:

Incorrect GST Return Reporting: Errors while filing GSTR-1 or GSTR-3B may affect turnover calculation.

Delayed Filing of Returns: Late filing can impact the GST Portal's auto-computed turnover.

Subsequent Amendments: Corrections made after the original return may create temporary mismatches.

Differences Between Accounting Records and GST Returns: Books of accounts and GST returns should always be reconciled to avoid discrepancies.

Incorrect Reporting of Exempt Supplies: Failure to report exempt supplies correctly may affect the Aggregate Annual Turnover.

Errors in Export Reporting: Incorrect reporting of zero-rated supplies can also result in turnover mismatches.

Multiple GST Registrations Under One PAN: Improper aggregation of turnover from different states may lead to inaccurate AATO.

Technical or Data Migration Issues: Occasionally, portal-related issues may also contribute to incorrect turnover figures.

Identifying these issues early helps businesses avoid unnecessary compliance complications.

Best Practices Before Submitting Your Amendment

Before submitting any amendment request, taxpayers should perform a thorough reconciliation of their records.

Reconcile Turnover with Audited Financial Statements

Ensure that the turnover reported on the GST Portal matches the audited financial records.

Compare GSTR-1, GSTR-3B, and Books of Accounts

Cross-verification helps identify inconsistencies before submission.

Verify Export Turnover

Confirm that all exports and zero-rated supplies have been reported correctly.

Review Exempt and Nil-Rated Supplies

Ensure that exempt transactions are properly reflected in the turnover.

Check Turnover Across All GST Registrations

Businesses with registrations in multiple states should verify that the combined turnover under the same PAN is accurate.

Identify Duplicate or Missing Transactions

Review sales records carefully to ensure that no transaction has been omitted or reported twice.

Maintain Supporting Documents

Keep reconciliation statements, financial records, invoices, and other supporting documents ready in case the tax officer seeks clarification during verification.

Key Dates Every Taxpayer Should Remember

|

Activity |

Date |

|

AATO Amendment Starts |

1 July 2026 |

|

Last Date to Amend |

31 July 2026 |

|

Tax Officer Verification |

1 August – 15 August 2026 |

Missing these dates means losing the current amendment opportunity for FY 2025–26.

Final Thoughts

The revised AATO amendment schedule may appear to be a minor procedural update, but its impact extends far beyond a simple date change. Aggregate Annual Turnover is a foundational data point used by the GST Portal to determine several compliance requirements, making its accuracy essential for every registered taxpayer.

With GSTN introducing enhanced system functionality that will automatically update turnover based on future GST returns, the government is moving towards a more automated and data-driven compliance ecosystem. This makes it even more important for businesses to ensure that their FY 2025–26 turnover details are correct before the amendment window closes.

Businesses should not wait until the last week of July. Reviewing turnover now, reconciling it with financial records, and making necessary corrections before 31 July 2026 can help avoid future compliance issues, unnecessary notices, and incorrect GST obligations.

Comments

No comments yet. Be the first to comment!