Direct Tax Collections FY 2025-26: What the Latest Income Tax Data Really Tells Us

The Income Tax Department of India has released the latest provisional figures for Gross Direct Tax Collections, Refunds, and Net Direct Tax Collections for FY 2025-26, reflecting the position as on 11 January 2026. These figures offer a timely and comprehensive view of the government’s revenue performance during the ongoing financial year and highlight how effectively the tax system is functioning.

Beyond headline numbers, the data serves as a key indicator of India’s fiscal health, revealing trends in taxpayer compliance, efficiency of tax administration, and the impact of policy measures implemented in recent years. It also provides early signals on how close the government is to achieving its annual revenue targets.

Interpreting this data is not relevant only for policymakers and economists. For businesses, professionals, and individual taxpayers, these trends carry practical implications ranging from stricter compliance monitoring and refund processing patterns to potential policy adjustments and enforcement priorities in the months ahead. Understanding what these numbers reflect can help taxpayers align their filing, accounting, and tax planning strategies with the evolving regulatory environment.

Understanding the Key Components of the Direct Tax Data Release

To correctly interpret the latest direct tax collection figures, it is essential to first understand the three core components highlighted in the data released by the Income Tax Department. Each of these components reflects a different aspect of the tax collection and administration process.

· Gross Direct Tax Collections

Gross Direct Tax Collections represent the total amount of direct taxes collected by the government before adjusting for any refunds. This includes revenue from:

- Corporate income tax paid by companies

- Personal income tax paid by salaried individuals, professionals, and self-employed taxpayers

- Securities Transaction Tax (STT) on equity market transactions

- Other direct taxes and statutory levies

Gross collections serve as a key indicator of economic activity, corporate profitability, employment levels, and overall income generation in the economy. A rise in gross collections generally signals stronger earnings and improved tax compliance across sectors.

· Refunds Issued

Refunds issued refer to the amounts returned to taxpayers when excess tax has been paid during the year. Refunds may arise due to:

- Excess TDS deducted by employers, banks, or other deductors

- Higher advance tax payments than the final tax liability

- Errors in tax computation corrected during assessment

- Legitimate refund claims processed after scrutiny

Refund trends are an important measure of filing accuracy, system efficiency, and data reconciliation quality. Lower or stable refund outflows often indicate better matching of TDS, AIS, and return data, while higher refunds may point to overpayment or filing mismatches.

· Net Direct Tax Collections

Net Direct Tax Collections are calculated after adjusting refunds from gross collections:

Net Direct Tax Collections = Gross Direct Tax Collections – Refunds Issued

This figure represents the actual tax revenue retained by the government and is the most critical metric for fiscal planning. It determines the government’s capacity to fund public expenditure such as infrastructure development, welfare schemes, defence spending, and debt servicing.

For policymakers, net collections reflect the true strength of the tax system. For taxpayers and businesses, trends in net collections often signal the likelihood of tighter compliance checks, enhanced scrutiny, and evolving tax enforcement priorities.

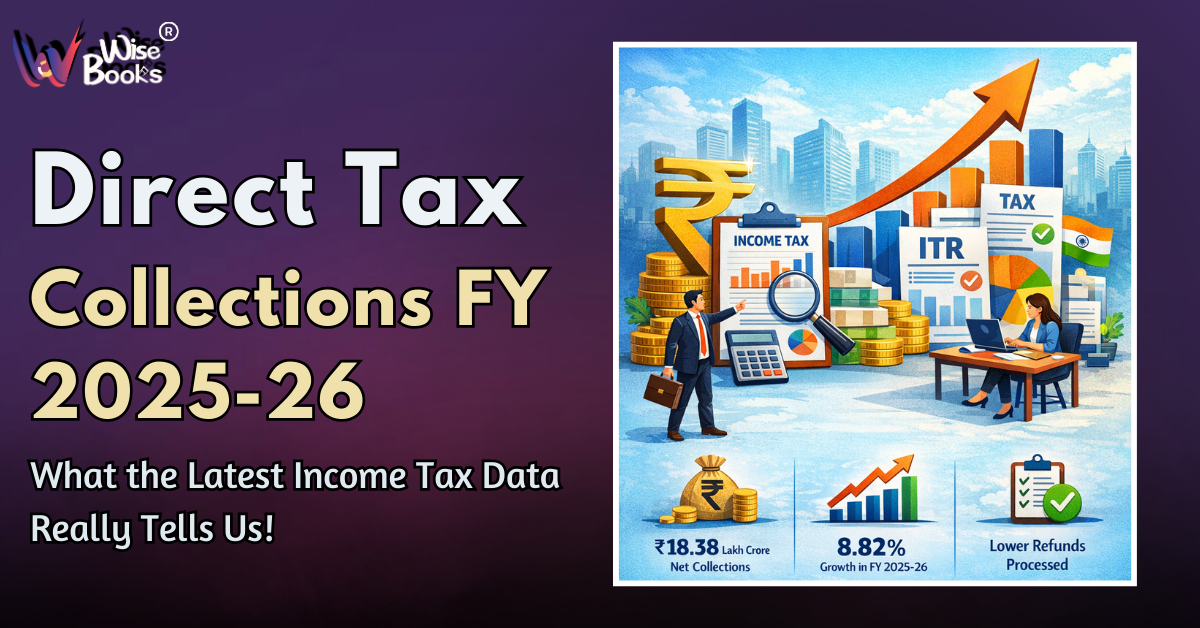

Key Highlights of FY 2025-26 Collections (As on 11 Jan 2026)

- Net direct tax collections have shown healthy year-on-year growth

- Gross collections continue to rise, though at a moderate pace

- Refund outflows are comparatively lower than the previous year

- Both corporate and non-corporate taxes have contributed to the increase

This combination has resulted in stronger net revenue performance, despite economic uncertainties.

Corporate Tax Performance: Stability Amid Economic Pressures

Corporate tax continues to be one of the largest contributors to India’s direct tax revenues, playing a crucial role in strengthening government finances. The stable performance observed in FY 2025-26 reflects both improved compliance practices and cautious but sustained business profitability across key sectors.

Why Corporate Tax Collections Remain Strong

Several structural and operational factors have supported steady corporate tax inflows:

1. Improved Profitability Among Large and Mid-Sized Companies

Many established companies have adapted well to changing market conditions through cost optimisation, digital transformation, and improved supply-chain management. This has helped maintain reasonable profit levels, directly supporting consistent corporate tax payments.

2. Stronger Compliance Through Digitisation

The Income Tax Department’s increasing use of:

- real-time data matching,

- AIS and TDS analytics, and

- system-generated risk profiling

has significantly reduced under-reporting and delayed tax payments. Businesses now operate in a more transparent environment, where discrepancies are quickly flagged.

3. Expansion of Faceless Assessments and Automated Reconciliation

Faceless assessment systems have improved efficiency and reduced manual intervention. Automated reconciliation of tax credits, advance tax, and financial statements has also minimised errors and disputes, leading to more predictable and timely tax collections.

Why Growth Remains Moderate, Not Aggressive

Despite the stability, corporate tax growth has been measured rather than rapid, mainly due to underlying business challenges:

1. Margin Pressure on MSMEs

Small and medium enterprises continue to face:

- rising input costs,

- higher borrowing expenses,

- delayed customer payments, and

- competitive pricing pressure

These factors limit profit expansion and, consequently, corporate tax growth from this segment.

2. Impact of Global Economic Slowdown

Certain industries such as exports, manufacturing, technology services, and logistics have been affected by slower international demand, geopolitical uncertainty, and currency fluctuations. These global factors constrain revenue growth and profitability, keeping tax contributions stable but not sharply higher.

What This Means for Businesses

This environment highlights a critical reality:

Corporate tax stability today depends more on compliance quality than aggressive profit growth.

Businesses must therefore prioritise:

- Accurate bookkeeping – clean financial records reduce assessment risks

- Timely tax provisioning – avoids interest and penalties

- Regular reconciliation of TDS, advance tax, and books

- Compliance discipline – timely filings, correct disclosures, and audit readiness

Companies with structured accounting systems and compliance planning are far better positioned to navigate scrutiny, avoid disputes, and maintain predictable cash flows.

Personal & Non-Corporate Tax Collections: Rising Compliance and Transparency

The continued growth in non-corporate tax collections covering salaried individuals, freelancers, professionals, and self-employed taxpayers reflects a significant shift in India’s tax compliance landscape. This upward trend indicates not just higher income reporting, but also deeper integration of technology into tax administration.

Key Drivers Behind the Rise in Non-Corporate Tax Collections

1. Higher Formalisation of Income

More individuals and professionals are operating within the formal economy due to:

- Increased digitisation of payments

- Mandatory PAN and Aadhaar linkage

- Widening reporting requirements across financial transactions

This has led to better visibility of income streams that were previously under-reported or untracked.

2. Expanded Reporting Through AIS, TDS & Digital Platforms

The introduction and continuous refinement of the Annual Information Statement (AIS), combined with TDS reporting and real-time data sharing by banks, employers, and financial institutions, has significantly reduced reporting gaps. Income details are now pre-populated and cross-verified, leaving little room for omission or misreporting.

3. Improved Monitoring of High-Value Transactions

High-value transactions such as property purchases, securities investments, large cash deposits, and foreign remittances are now systematically tracked. This enhanced surveillance has strengthened compliance and increased voluntary disclosures among taxpayers.

As a result, the scope for under-reporting income has narrowed considerably, making accurate ITR filing not just advisable, but essential to avoid mismatches, notices, and penalties.

Refund Trends: What the Decline in Refund Outflows Indicates

Another key takeaway from the latest data is the decline in refund outflows compared to the previous financial year. This trend has played a crucial role in strengthening net direct tax collections.

Why Refunds Have Reduced

Several systemic improvements have contributed to this decline:

1. Better Matching of TDS, AIS & ITR Data

Advanced data analytics now enable precise matching between tax deducted at source, income disclosures, and filed returns. This has reduced instances of excess tax payments and incorrect refund claims.

2. Reduction in Erroneous Refund Claims

Improved pre-filing data and system validations have helped curb refund claims arising from calculation errors, duplicate credits, or ineligible deductions.

3. Stricter Scrutiny of High-Value Refunds

Large refund claims are increasingly subjected to additional verification and risk-based checks, ensuring that only genuine refunds are processed.

4. Use of Risk-Based Review Systems

The department’s shift towards risk profiling and automated alerts has enhanced efficiency while preventing revenue leakage, contributing to controlled refund outflows.

What This Means for Government Finances

· Progress Toward Budget Targets

The strong performance in net direct tax collections indicates that the government is well positioned to meet or potentially exceed its direct tax targets for FY 2025-26, provided economic activity remains stable in the remaining months of the financial year. Consistent revenue inflows reduce reliance on additional borrowing and improve confidence in fiscal planning.

This progress also strengthens the government’s ability to maintain predictable expenditure patterns without resorting to sudden policy adjustments or mid-year fiscal tightening.

· Strengthening Fiscal Discipline

Healthy and sustained tax revenues give the government greater financial flexibility, allowing it to:

- Manage the fiscal deficit more effectively by balancing expenditure with reliable revenue inflows

- Increase spending on infrastructure projects, which support long-term economic growth

- Fund welfare and social development programs without excessive borrowing

- Maintain macroeconomic stability, which helps control inflation and preserve investor confidence

Overall, stronger tax collections enhance fiscal resilience and provide policymakers with greater room to respond to economic challenges.

What This Means for Taxpayers & Businesses

1. Expect Tighter Scrutiny Going Forward

Historically, higher tax collections are often followed by more intensive compliance monitoring. As revenue targets come within reach, tax authorities tend to focus on improving the quality of filings rather than expanding the tax base alone. This may result in:

- Increased scrutiny of income tax returns

- A rise in system-generated notices for mismatches or inconsistencies

- Greater emphasis on data accuracy and disclosure completeness

Taxpayers should therefore be prepared for a more vigilant compliance environment.

2. Accurate Filing Is No Longer Optional

With advanced analytics and automated validations in place, even minor discrepancies can trigger queries. To minimise risks, taxpayers must ensure:

- Selection of the correct ITR form based on income type and status

- Complete disclosure of all income sources, including interest, capital gains, and digital income

- Proper reconciliation of TDS, GST, and accounting records before filing

Accuracy at the time of filing significantly reduces the likelihood of notices, delays, and litigation.

3. Growing Importance of Professional Accounting Support

For businesses in particular, clean and well-maintained financial records have become a critical compliance advantage. Organisations with structured bookkeeping and reconciled data typically experience:

- Fewer compliance-related notices

- Faster processing of refunds

- Lower exposure to assessments and disputes

As tax administration becomes increasingly automated, professional accounting and compliance support is no longer a luxury, it is a necessity for sustainable business operations.

Conclusion

The provisional direct tax data for FY 2025-26 (as on 11 January 2026) underscores a tax system that is becoming stronger, more efficient, and increasingly transparent. With rising net collections, controlled refund outflows, and consistent contributions from both corporate and non-corporate taxpayers, the figures reflect not only healthy revenue performance but also the impact of technology-driven compliance and data analytics in modern tax administration.

For taxpayers and businesses, the message is clear: accuracy, structured bookkeeping, and timely filing are no longer optional, they are essential. In an environment of stricter scrutiny, automated validations, and risk-based assessments, proactive tax management and proper reconciliation of accounts can help avoid notices, reduce delays in refunds, and minimise disputes.

At the same time, these trends signal the government’s growing fiscal stability and capacity to fund infrastructure, welfare programs, and economic growth initiatives without over-reliance on borrowing.

Comments

No comments yet. Be the first to comment!