Introduction

In a significant and taxpayer-friendly ruling, the Allahabad High Court has reaffirmed the fundamental principle of natural justice under GST law. The Court held that once a taxpayer’s GST registration is cancelled, they cannot be expected to regularly monitor the GST portal for notices.

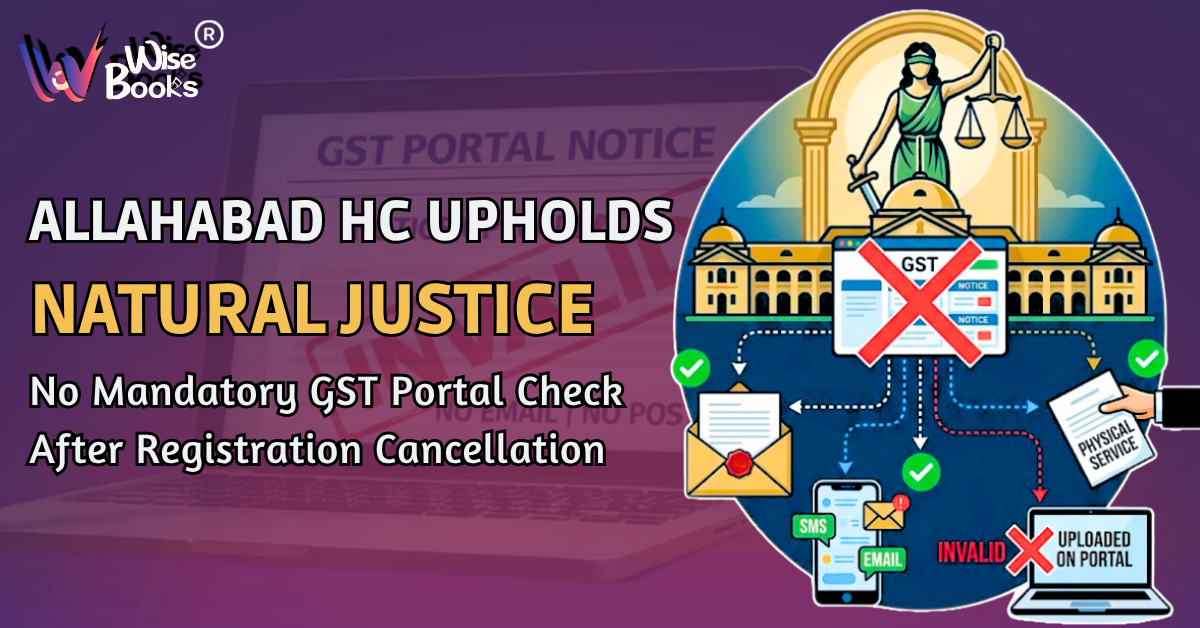

Further, the Court clarified that mere uploading of a notice on the GST portal does not constitute valid service of notice, especially when no additional communication is made through prescribed modes.

Background of the Case

In the present case, the taxpayer’s GST registration had already been cancelled. Subsequently, the GST department issued a Show Cause Notice (SCN) and initiated proceedings.

However, the notice was:

- Uploaded only on the GST portal

- Not communicated via email, SMS, or physical delivery

The taxpayer challenged the proceedings on the ground that:

- They were not properly informed

- They had no opportunity to respond

- The entire process violated principles of natural justice

Court’s Observations

The Allahabad High Court made the following important observations:

- A taxpayer cannot be expected to check the GST portal regularly after cancellation of registration

- Authorities must ensure that notices are served through legally recognized modes of communication

- Uploading notices only on the portal is insufficient and improper service

The Court referred to provisions governing service of notice, which require communication through multiple channels such as:

- Registered email

- SMS alerts

- Physical delivery or post

Violation of Natural Justice

The Court emphasized that the essence of natural justice lies in:

- Providing proper notice

- Granting a fair opportunity to be heard

In this case:

- No proper notice was served

- No real opportunity was given to the taxpayer

Therefore, the Court held that the entire proceedings were vitiated due to violation of natural justice.

Judgment

Based on the above findings, the Allahabad High Court:

i. Quashed the GST Order

The Allahabad High Court cancelled the GST order because it was passed without proper notice, violating principles of natural justice.

ii. Allowed Fresh Proceedings

The Court permitted the department to start the case again, meaning the matter is not closed but can be reconsidered as per law.

iii. Proper Notice Mandatory

The Court directed that, this time, authorities must serve notice through valid legal modes (not just the portal) to ensure the taxpayer gets a fair opportunity to respond.

Key Legal Principles Established

- Portal upload alone is not valid service of notice

- After cancellation, checking GST portal is not mandatory

- Natural justice must be strictly followed in GST proceedings

Practical Implications

For Taxpayers

- Relief from the burden of continuously checking the GST portal after cancellation

- Protection against unfair or ex-parte orders

For Professionals (CA / Tax Advisors)

- Strong legal ground to challenge invalid GST notices

- Useful precedent in litigation and advisory matters

Conclusion

This judgment reinforces that procedural fairness is essential in tax administration. The Allahabad High Court has made it clear that:

i. Proper service of notice is not a mere formality but a legal necessity

ii. Technical compliance cannot override the principles of natural justice

Tax authorities must ensure that taxpayers are properly informed and given a fair chance to respond before passing any adverse order.

Comments

No comments yet. Be the first to comment!